By MATTHEW HOLT

There’s been plenty of dialogue recently about whether or not digital well being is a respectable place for enterprise capital. There have been plenty of large failures, only a few notable successes (and positively no “biggest companies in the world” but), whereas some actual giants (Walmart/Walgreens/Amazon) have are available after which received out of well being care.

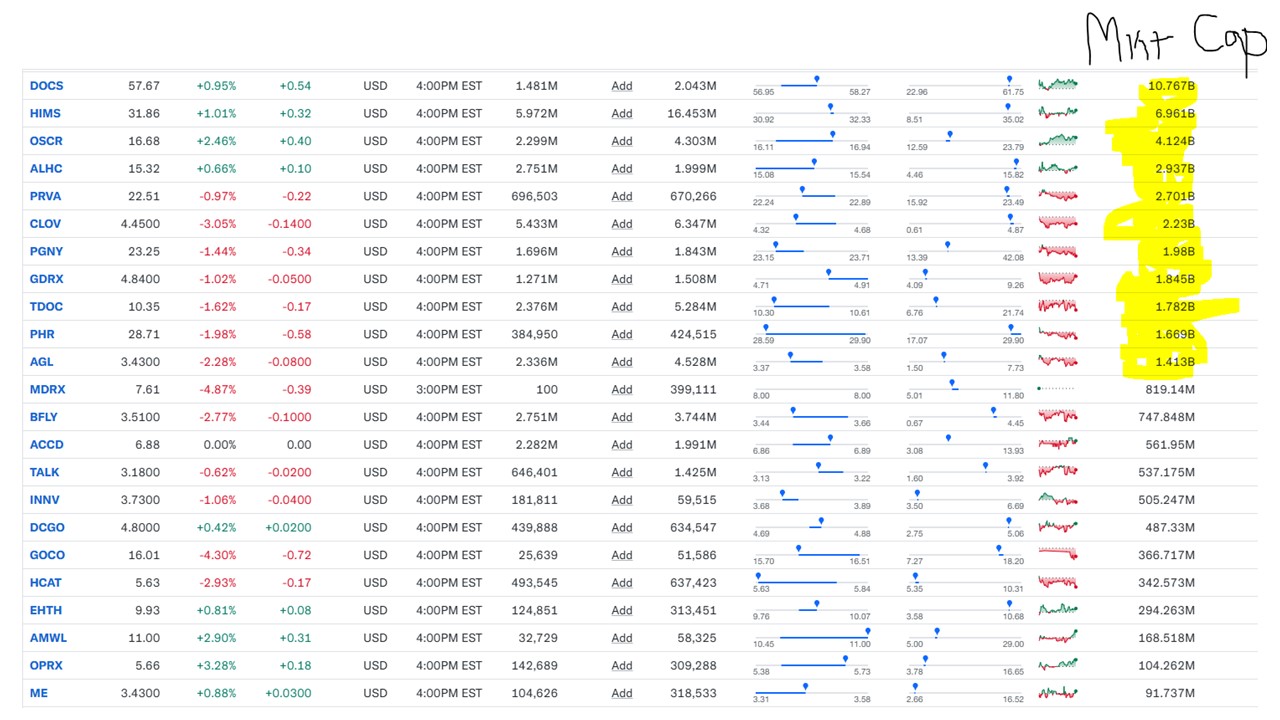

I don’t must inform you once more that many of the publicly traded digital well being corporations are buying and selling at pennies on the greenback to their preliminary valuations. However I’ll. Take a look at that chart beneath.

Heck even Doximity– which prints cash (45% internet margins!)–is buying and selling at properly beneath its submit IPO excessive. My fast overview is that there are usually not very many publicly traded corporations at unicorn standing. With actually solely Doximity, HIMS and Oscar being very profitable. (We are able to have a separate argument as as to whether Tempus and Waystar are “digital well being”). And there are various, many which might be properly off the worth they IPOed at. All that at a time when the common inventory market is hitting document highs.

Which makes it attention-grabbing to say the least that Outline Ventures simply came out with a report saying that usually digital well being has executed properly as a enterprise funding and that it was prone to do even higher, quickly.

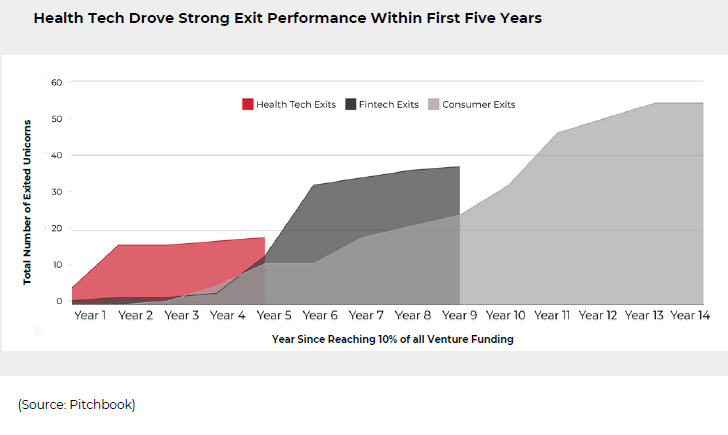

The report isn’t that lengthy and is properly value a learn however their fundamental argument compares digital well being enterprise investments to these in fintech and shopper tech. Basically it took digital well being quite a bit longer to get to 10% of complete enterprise funding than fintech or shopper tech, however it received there after 2020. Now greater than 10% of all VC backed unicorns on the market are well being tech corporations. Sure there was a retrenchment in 2022-3 however well being tech funding fell much less than different sectors in 2022-3 and is mainly again in 2024.

The Outline forecast forecast is attention-grabbing (it’s the chart beneath). Outline posits that it took 4-5 years after the fintech and shopper tech sectors turned 10% of VC {dollars} for them to start out pumping out exits and IPOs. There are 30-50 every in these sectors now, however well being tech was forward of that with 18 exits already within the first 5 years after attending to 10% of VC {dollars}, and people exits have been on common double the dimensions of the fintech/shopper tech exits. (Though to be truthful the well being tech exits have been when the market was greater after 2020)

In truth their evaluation is that capital returned was about 10x funding. You may say, however hey Matthew didn’t you simply present me a chart that almost all of these 18 corporations have been public market canine? And also you’d be proper.

If we take a look at the 18 corporations Outline examines, they don’t truly match the listing of 11 unicorns I’ve on my chart earlier however usually they haven’t executed properly in the long term.

Some have gone beneath (Science 37 & NueHealth bought for components), some have been purchased for actual cash, if approach lower than they as soon as traded for (One Medical was at one level $50 a share however purchased for $18, however that was $3.9 billion together with debt, Accolade was simply purchased by Transcarent for about $600m), whereas most have slowly declined to properly lower than IPO value (Amwell, Talkspace, Well being Catalyst, and all of the bits at present inside Teladoc, together with Livongo & InTouch).

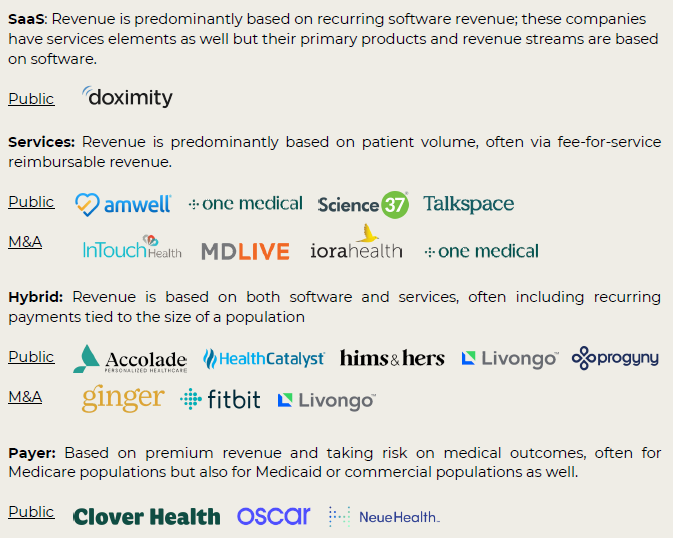

However Outline in contrast these public corporations’ efficiency to another unprofitable early stage public corporations and noticed that these corporations they outlined as “companies” and “payers” did worse however “hybrid” and “SaaS” did higher than different tech corporations.

(By the best way, it’s fairly wonderful that somebody put collectively an index of loss making public tech corporations however apparently Morgan Stanley did! It’s known as MSUPTX though my Googling can’t discover it!)

Outline can also be suggesting that the subsequent set of digital well being corporations to go public or exit through M&A will accomplish that quicker and at a better worth. Typically that’s as a result of “element components tech” is extra simply available for purchase off the shelf, with AI being the plain “element” instance. Subsequently these corporations will get to scale faster, and AI will speed up that. Right here’s their listing, which incorporates one companies firm, Carebridge, that already had exit.

However I’m nonetheless extremely involved that these corporations can’t get to a smart valuation based mostly on what they’ve raised. Let’s evaluate them to the darling of what Outline calls “Wave 1” of well being tech IPOs. Livongo raised $237m before its IPO. Okay that’s not rooster feed however it was valued beneath $1bn earlier than the IPO and round $4bn quickly after the IPO. 3 months later it was buying and selling again down nearer to $2bn after which started its pandemic-fueled rise to a $20bn market cap and the well-known $19bn merger with Teladoc.

$237m might sound like quite a bit for complete capital raised however Innovacer has raised $675m, Lyra & Hinge Well being almost $1bn every, Included Well being’s element components have raised “solely” $500m, and Devoted Well being has raised over $2.25bn. So these corporations are going to must get out at multi-billion greenback valuations to do something like in comparison with Livonogo’s success, after which public market traders (or their buying corporations within the case of M&A) are going to count on them to develop from there. Given the efficiency of the businesses within the sector now, and that there are nonetheless many related corporations value a complete lot much less on the general public market, both these personal corporations have some large efficiency occurring, otherwise you’d think about they’ll disappoint their traders.

So how can Outline declare that the primary wave of corporations returned 10 occasions the capital invested?

I believe that’s comparatively easy.

A lot of these corporations IPOed or have been acquired at a value properly in extra of the place they ended up. However should you have been an early stage investor capable of promote on the IPO or shortly after, you might properly have made that ten bagger return.

Perhaps should you invested early sufficient within the second wave, you may see that return too. However so a lot of these corporations raised a lot cash at such a excessive valuation within the halcyon days of 2021 & early 2022 (to not point out late 2024 and early 2025) that it’s onerous to see these ranges of returns for many traders. And naturally in case you are a public market investor shopping for within the frothy interval post-IPO, the prospect that you just’re a pig being led to slaughter could be very excessive certainly.

However should you’re a VC and you should buy in low-cost sufficient you may make nice returns. As long as you do your inventory buying and selling rigorously, and have some luck!

Source link

{kind=link}

{kind=link}